Are Flexible Spending Accounts Killing Your Retirement Benefits?

- March 19, 2019

- by Michael

Flexible spending accounts give you a tax break in the short term but come with some drawbacks, including the fact that they reduce your social security benefits. We ran the numbers and went in depth to help you determine if an FSA makes sense.

You’ve probably heard about flexible spending accounts, which can be used either for medical expenses like copays and deductibles or for dependent care, like preschool. They go by acronyms like Dependent Care Assistance Program (DCAP), Health Reimbursement Arrangement (HRA), Medical Expense Reimbursement Plan (MERP), etc.

Flexible spending accounts can save you a lot of money now, because the money you put in is “pre-tax”. In other words there are no income taxes or social security taxes taken out of the cash you put into a flexible spending account.

There are three major downsides to flexible spending accounts (FSA):

The first is that if you put money aside and then don’t spend it, you lose the money. Most people understand that trade-off and have a good idea of how much they will spend in the next year. In some cases you may be able to roll a portion of unspent money into the next year.

The second downside of FSAs is the extra work it takes to understand the rules and file for reimbursements to actually get the benefit. With FSAs there is a narrow set of allowed expenses. The program guide will explain how it works. For example, with a DCAP account you can’t purchase a laptop for your child. You may only spend DCAP money on care for your child, such as at a licensed daycare. Keeping track of receipts, dealing with filing the paperwork and putting up with disputes can be a real time suck.

The third downside is less well-known, and essentially hidden. Because contributing to a flexible spending account reduces your income for social security benefits, it decreases your monthly benefit amount in retirement.

Let’s dig into that last fact a lot more. As with everything related to social security and taxes, it’s complicated and the best step for you depends on your overall income and financial situation. That’s because your tax rate is different depending on how much you earn. The way the math works high earners benefit much more from tax deferral than low earners do.

Social security benefits, especially how income counts towards credits, is really complicated. 90% of your monthly earnings up to $926 are counted towards your social security benefits, but only 15% of earnings over $5,583 count towards social security benefits. So high earners have much less to lose in terms of social security benefits than low-earners do. Here’s another link to explain how social security benefits are calculated.

What does this mean? The more you earn, the more likely an FSA is a good trade-off. For many families, though, it comes down to having money now (which, to be fair, you could invest and see better returns) or having money later.

Scenario 1 - High Earner:

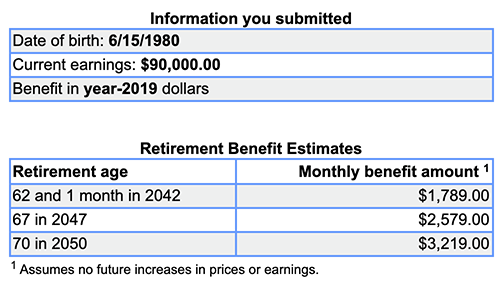

For our first scenario, let’s consider a person born in 1980 who plans on retiring at age 70 and earns $90,000 per year (indexed to inflation).

To run the calculation yourself, try the Social Security Quick Calculator Tool.

With no contributions to an FSA she will be eligible for $3,219 in monthly benefits.

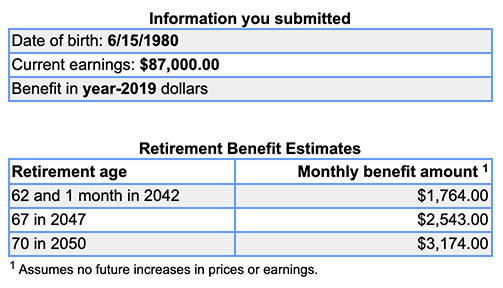

With a $3,000 annual FSA contribution that lowers her income to $87,000 for social security credit purposes. After retiring at age 70, she will get only $3,174 in monthly benefits, $45 less than if she hadn’t used the FSA.

At marginal tax rate of 25% she will save $750 / year (or $62.50 / month) in taxes by using a FSA.

So by using the FSA, a person earning $90k / year will save $62.50 per month in today’s money (by not having to pay that in taxes), but in retirement her benefit is reduced by $45 per month. The reduction is less if she retires earlier (say age 62 instead of 70).

In addition if she saves that $62.50 per month and invests it, assuming a 5% rate of return, she will have an additional $49,829 of net worth 30 years later (in today’s dollars). Assuming a 4% withdrawal rate, she could take out ~$2000 per year, which averages out to about $166 per month, more than making up for her lost $45 in social security benefits, by $121.

Scenario 2 - Average Earner:

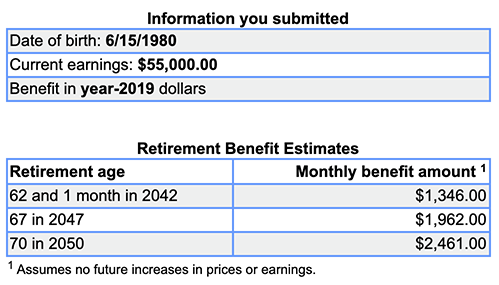

For our second scenario, let’s consider the same person - born in 1980 who plans on retiring at age 70, except they earn $55,000 per year (indexed to inflation).

With no contributions to an FSA she will be eligible for $2,461 in monthly benefits.

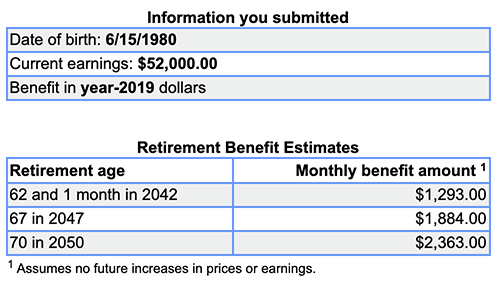

With a $3,000 annual FSA contribution that lowers her income to $52,000 for social security credit purposes. After retiring at age 70, she will get only $2,363 in monthly benefits, $98 less than if she hadn’t used the FSA.

At marginal tax rate of 15% she will save $450 / year (or $37.50 / month) in taxes by using a FSA.

So by using the FSA, a person earning $55k / year will save $37.50 per month in today’s money (by not having to pay that in taxes), but in retirement her benefit is reduced by $98 per month. The reduction is less if she retires earlier (say age 62 instead of 70).

In addition if she saves that $37.5 per month and invests it, assuming a 5% rate of return, she will have an additional $29,897 of net worth 30 years later (in today’s dollars). Assuming a 4% withdrawal rate, she could take out ~$1600 per year, which averages out to about $133 per month, which does make up for her lost $98 in social security benefits, but only by $35.

Given the assumptions we made, the numbers from the social security quick calculator, and including saving and investing the tax break, the average earner gets only 20% of the benefit the high earner gets.

So what we see again is, thanks to the way the US tax code works, the more a person earns the easier it is to save at a higher rate.

The exact tax savings will depend on your filing status, if you’re married, if you have children, how much you earn, and when you retire. Generally speaking the higher your income, and the longer you wait to draw social security, the more likely that FSAs will make long-term financial sense.

Is an FSA account right for you? Play around with the Social Security Quick Calculator Tool, our Compound Interest Calculator, and if you are really into the numbers try our Income Spending Simulator to see how you would come out.